From its rich history to its prime location and abundance of amenities, Fairfield offers an unparalleled quality of life for residents of all ages. Whether you're seeking a close-knit community, access to outdoor recreation, or proximity to urban centers, Fairfield has it all.

FOR SALE

→ 67 Zinnia Lane

$699,000

Napa

67 Zinnia Lane

4 Bedrooms | 3 Baths | 2,714 sq. ft.

Offered for: $699,000

Click to turn the page below and read this homes story↴

Click to turn the page below and read this homes story↴

- MLS#: 325025229

- 4 Bedrooms

- 3 Baths

- Living Space: 2,714 sq. ft.

- Lot Size: +/-.25 Acre

- Year Built: 1992

- Subdivision: Circle Oaks

- Levels: Multi Levels

- APN: 032-320-017-000

- Garage: Two Car

- HOA: Yes

- Roof: Composite

- Water Source: Water District

- Sewer Source: Connected

- Wood Stove

- Remodeled

- Newer Bathrooms

- Stainless Steel Appliances

- Two Rear Decks

- HVAC

Welcome to 67 Zinnia Ln, a beautifully updated 4-bedroom, 3-bathroom home offering 2,714 sq. ft. of living space on a spacious 0.25-acre lot in Napa's serene Circle Oaks community. Built in 1992, this residence features an open floor plan with a cozy wood-burning stove and a spacious kitchen. Recent updates enhance its charm, with large windows inviting abundant natural light. The bathrooms are a standout, boasting heated floors for added comfort and Toto self-cleaning toilets that elevate modern living.

The finished lower level includes a kitchenette and a separate entrance, making it ideal for multi-generational living or potential rental income. Two expansive decks provide stunning countryside views, while the generous backyard offers ample space for gardening, outdoor activities, or entertaining. This move-in-ready home seamlessly blends modern updates with peaceful country living.

About the Circle Oaks Community:

Nestled in the hills east of Napa Valley, Circle Oaks is a unique, unincorporated community established in 1964. Known for its distinctive circular lots, each approximately 1/4 acre, the design preserves greenbelt areas between properties, fostering a harmonious connection with nature.

Residents enjoy a tranquil, wooded environment teeming with wildlife, offering a peaceful retreat from the bustle of city life. Despite its secluded feel, Circle Oaks is conveniently located about 10 miles from downtown Napa, providing easy access to shopping, dining, and world-renowned wineries. The community is also a short drive from recreational opportunities at Lake Berryessa, perfect for boating and outdoor enthusiasts.

Managed by the Circle Oaks Homeowners Association, the community maintains a commitment to enhancing residents' living experiences through various amenities and services. Regular events and meetings foster a close-knit neighborhood atmosphere, making Circle Oaks not just a place to live, but a place to belong.

Don't miss this opportunity to own a piece of this serene and distinctive community. Schedule a showing today!

WHO YOU WORK WITH MATTERS

A new market to navigate, a new way to buy and sell,

a new way home.

The language of home is universal. It is the place where you are most known and most comfortable, where life unfolds and your story begins. Home is where you discover the extraordinary in the everyday. At Navigate Real Estate, we believe that "Every home has a story," and our mission is to help you tell yours. No matter where you are in your journey, Navigate Real Estate is an invaluable ally in your home buying and selling experience.

Wherever you're going... We'll get you there!

We see home as more than a house, so we approach real estate as more than a transaction. It's how we build relationships - by making people feel happy and confident about the biggest investment of their lives. This is more than our profession; it's our passion because our family never forgets how much home truly means to you and your family. So when you're ready for your next moment or your next adventure, call Alicia, she'll help you get there.

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

GOT QUESTIONS?

Get in Touch With Alicia

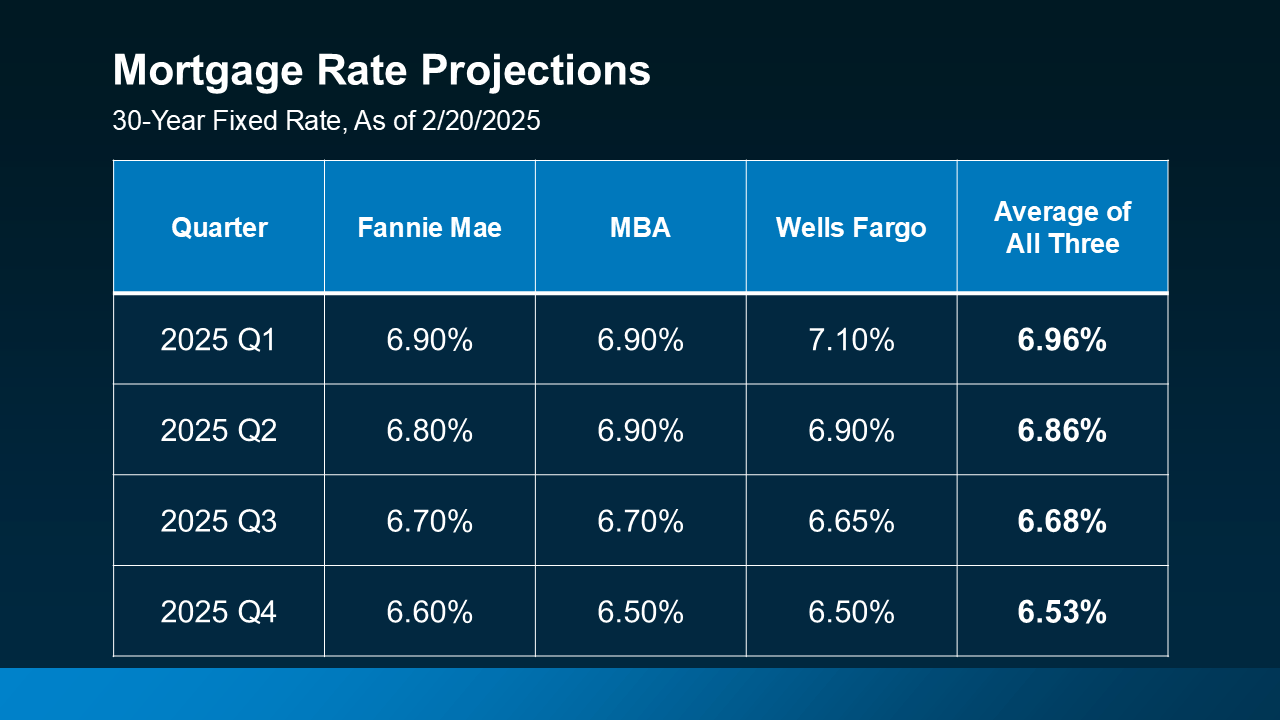

Many people are hoping mortgage rates will come down before they buy a home. But will that actually happen? According to the latest forecasts, experts say rates will decline, but not by as much as a lot of people want.

The good news? Even if they don’t drop substantially, there are still ways to make buying a home more affordable.

How Much Will Rates Drop?

A few months ago, experts were forecasting mortgage rates could dip below 6% by the end of the year. But recent projections suggest that may not happen after all.

While mortgage rates are still expected to decline some later this year, projections from Fannie Mae, the Mortgage Bankers Association (MBA), and Wells Fargo now show them stabilizing closer to the 6.5% to 7% range (see below):

That means if you’re holding off on buying a home in hopes of much lower mortgage rates, you may be waiting a while. And if you need to move because something in your life has changed, like a new job, a new baby, or a marriage – waiting that long may not be an option.

That means if you’re holding off on buying a home in hopes of much lower mortgage rates, you may be waiting a while. And if you need to move because something in your life has changed, like a new job, a new baby, or a marriage – waiting that long may not be an option.

Creative Financing Options in Today’s Market

Since rates aren’t expected to decline as much as originally expected, it may be worth considering alternative financing options that could help you get into a home sooner rather than later. Here are three strategies to discuss with your lender to see if any of these make sense for you:

1. Mortgage Buydowns

A mortgage buydown allows you to pay an upfront fee to lower your mortgage rate for a set period of time. This can be especially helpful if you want or need a lower monthly payment early on. In fact, 27% of agents say first-time homebuyers are increasingly requesting buydowns from sellers in order to buy a home right now.

2. Adjustable-Rate Mortgages

Adjustable-rate mortgages (ARMs) typically start with a lower mortgage rate than a traditional 30-year fixed mortgage. This makes them an attractive option, especially if you expect rates to drop in the coming years or plan to refinance later.

And if you remember the housing crash, know that today’s ARMs aren’t like the risky ones back then. Lance Lambert, Co-Founder of ResiClub, helps drive this point home by saying:

“. . . ARM products today are different from many of the products issued in the mid-2000s. Before 2008, lenders often approved ARMs based on borrowers ability to pay the initial lower interest rates. And sometimes they didn’t even check that (remember Ninja loans). Today, adjustable-rate borrowers qualify based on their ability to cover a higher monthly payment, not just the initial lower payment.”

In simple terms, banks used to give loans without checking to see if buyers could afford them. Now, lenders verify income, assets, and jobs, reducing the risks associated with ARMs compared to the past.

3. Assumable Mortgages

An assumable mortgage allows you to take over the seller’s existing loan — including its lower mortgage rate. And with more than 11 million homes qualifying for this option according to U.S. News, it’s worth exploring if you want or need a better rate.

Bottom Line

Waiting for a big decline in mortgage rates may not be the best strategy. Instead, options like buydowns, ARMs, or assumable mortgages could make homeownership more affordable right now. Connect with a local lender to explore what works for you.

How does this impact your homebuying plans this year?

Some homeowners hesitate to sell because they’ve got unanswered questions that hold them back. But a lot of times their concerns are based on misconceptions, not facts. And if they’d just talk to an agent about it, they’d see these doubts aren’t necessarily a hurdle at all.

If uncertainty is keeping you from making a move, it’s time to get the real answers. The ones you deserve. And to take the pressure off, you don’t have to ask the questions, because here’s the data that answers them.

1. Is It Even a Good Idea To Move Right Now?

If you own a home already, you may be tempted to wait because you don’t want to sell and take on a higher mortgage rate on your next house. But your move may be a lot more feasible than you think, and that’s because of how much your house has likely grown in value.

Think about it. Do you know anyone in your neighborhood who’s sold their house recently? If so, did you hear what it sold for? With how much home values have gone up in recent years, the number may surprise you. According to Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), the typical homeowner has gained $147,000 in housing wealth in the last five years alone.

That’s significant – and when you sell, that can give you what you need to fund your next move.

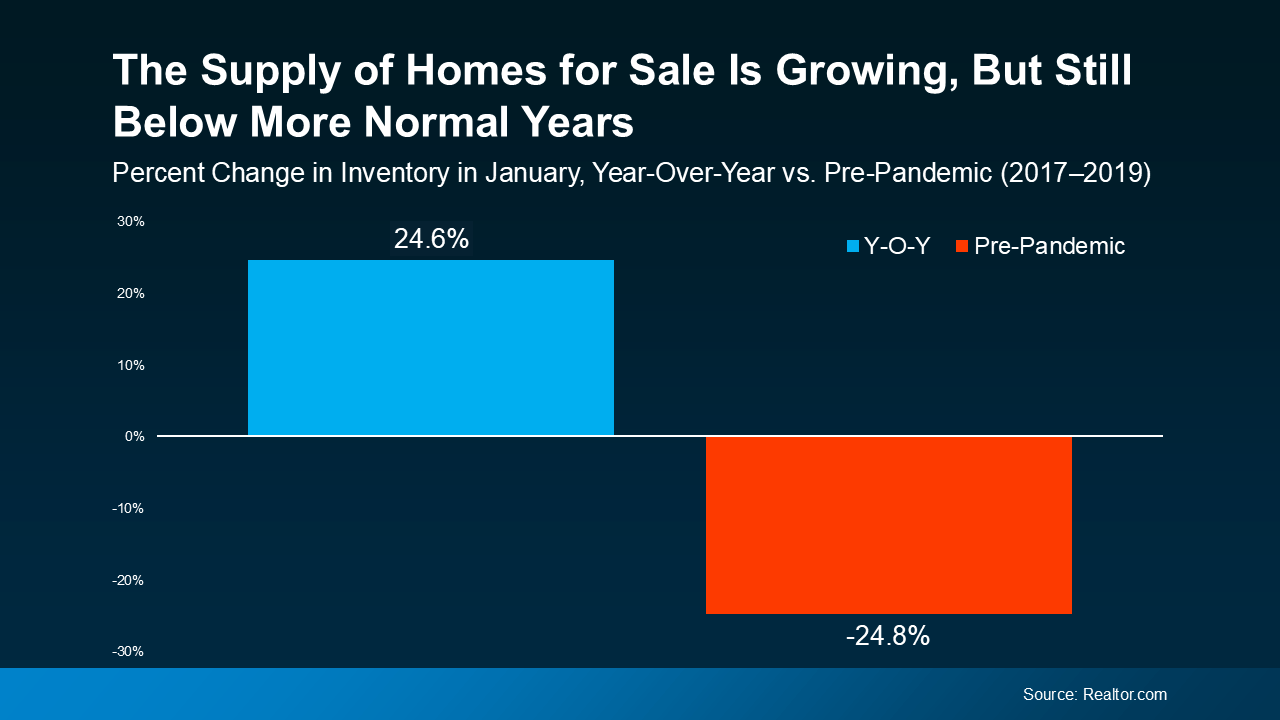

2. Will I Be Able To Find a Home I Like?

If this is on your mind, it’s probably because you remember just how hard it was to find a home over the past few years. But in today’s market, it isn’t as challenging.

Data from Realtor.com shows how much inventory has increased – it’s up nearly 25% compared to this time last year (see graph below):

Even though inventory is still below more normal pre-pandemic levels, it’s improved a lot in the past year. And the best part is, experts say it’ll grow another 10 to 15% this year. That means you have more options for your move – and the best chance in years to find a home you love.

Even though inventory is still below more normal pre-pandemic levels, it’s improved a lot in the past year. And the best part is, experts say it’ll grow another 10 to 15% this year. That means you have more options for your move – and the best chance in years to find a home you love.

3. Are Buyers Still Buying?

And last, if you’re worried no one’s buying with rates and prices where they are right now, here’s some perspective that can help. While there weren’t as many home sales last year as there’d be in a normal market, roughly 4.24 million homes still sold (not including new construction), according to the National Association of Realtors (NAR). And the expectation is that number will rise in 2025. But even if we only match how many homes sold last year, here’s what that looks like.

- 4.24 million homes ÷ 365 days in a year = 11,616 homes sell each day

- 11,616 homes ÷ 24 hours in a day = 484 homes sell per hour

- 484 homes ÷ 60 minutes = 8 homes sell every minute

Think about that. Just in the time it took you to read this, 8 homes sold. Let this reassure you – the market isn’t at a standstill. Every day, thousands of people buy, and they’re looking for homes like yours.

Bottom Line

When you’re ready to walk through what’s on your mind, I have the answers you need. And in the meantime, tell me: what’s holding you back from making your move?

Have you been wondering whether you should keep renting or finally make the leap into homeownership? It’s a big decision, and let’s be real — renting can feel like the easier option, especially if buying a home feels out of reach.

But here’s the thing: a recent report from Bank of America highlights that 70% of prospective buyers fear the long-term consequences of renting, including not building equity and dealing with rising rents.

Maybe you’re feeling that too — concerned about where renting might leave you down the road, but still unsure if you’d even be able to buy right now. The truth is, if you’re able to make the numbers work, buying a home has powerful long-term financial benefits.

Let’s break down why homeownership is worth considering in 2025 and beyond, and how it can help set you up for the future.

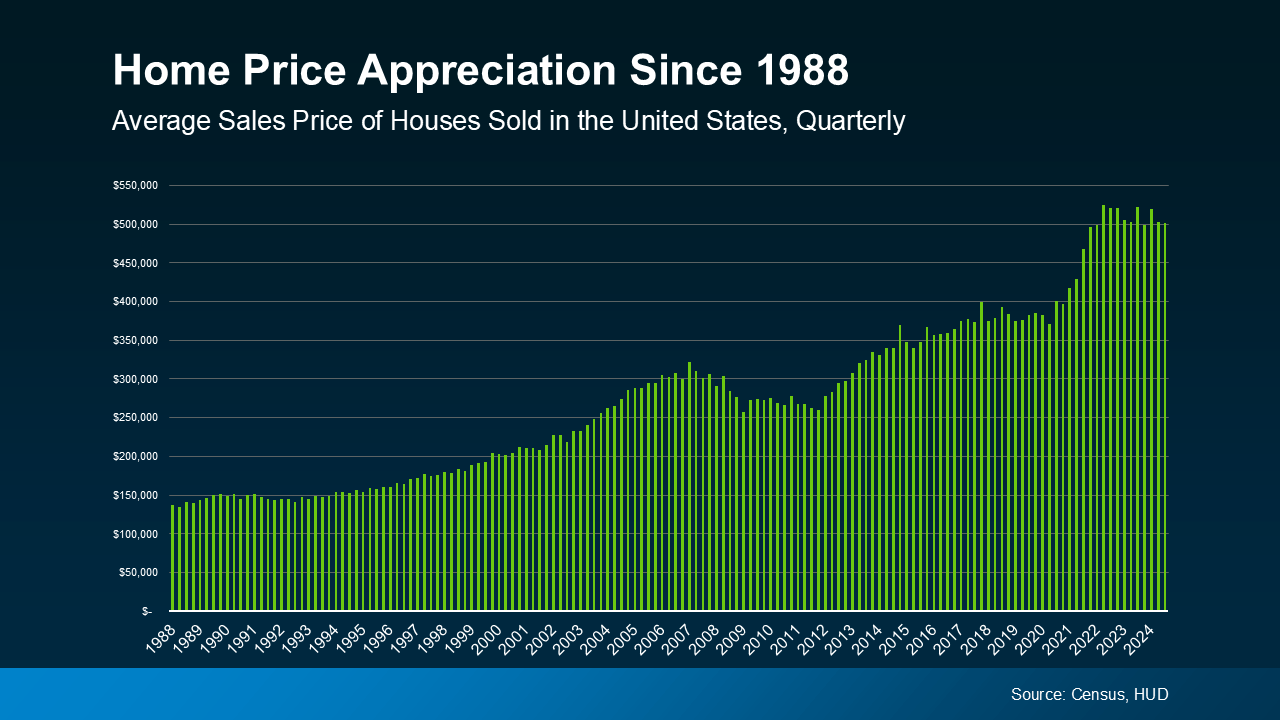

Buying Builds Wealth Over Time

Buying a home allows you to turn your monthly housing costs into a long-term investment. That’s because, as shown in data from the Census and the Department of Housing and Urban Development (HUD), home prices tend to increase over time (see graph below):

Rising home prices directly benefit homeowners. That’s because when you own a home, you build equity — meaning your ownership stake in your home grows as you pay down your mortgage and your home’s value appreciates. And that, in turn, makes your net worth grow too.

Rising home prices directly benefit homeowners. That’s because when you own a home, you build equity — meaning your ownership stake in your home grows as you pay down your mortgage and your home’s value appreciates. And that, in turn, makes your net worth grow too.

Maybe that’s why, according to the National Association of Realtors (NAR), 79% of buyers believe owning a home is a good financial investment.

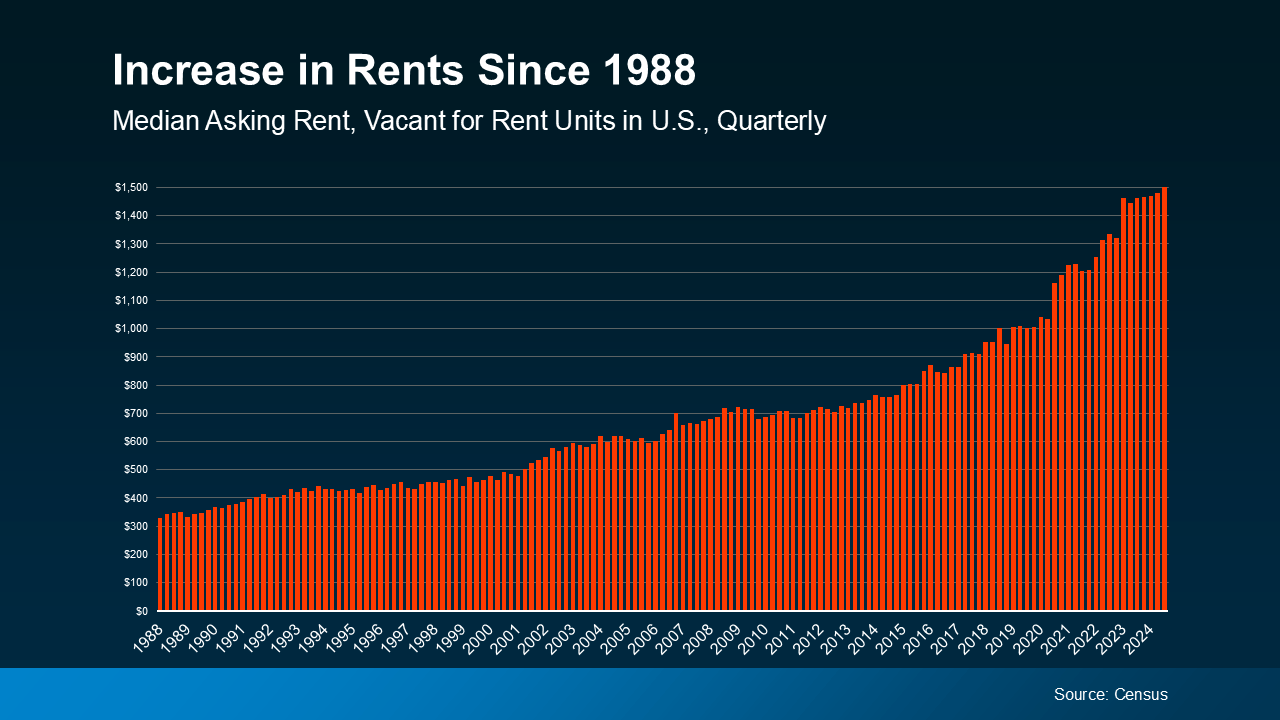

Renting Comes with Rising Costs

Renting may feel more affordable in the short term, especially right now with today’s home prices and mortgage rates. But the reality is, over time, rent almost always goes up too. Take a look at the data and you can see that play out. According to Census data, rents have significantly increased over the decades (see graph below):

This means if you decide to rent, you’ll likely face growing expenses each time you renew or sign a new lease – and that’ll happen without building any wealth in return. Plus, those rising costs may make it harder to save up to buy a home down the road.

This means if you decide to rent, you’ll likely face growing expenses each time you renew or sign a new lease – and that’ll happen without building any wealth in return. Plus, those rising costs may make it harder to save up to buy a home down the road.

Renting vs. Buying: The Long-Term Impact

When you own a home, your payments are an investment in your future. Renting, on the other hand, means your money is gone for good — it helps your landlord build equity, not you.

Renting works for those not ready (or able) to buy today. But if you are able to make the numbers work, buying a home builds equity and sets you up for long-term financial success. So, even though renting may seem easier now, it can’t match the benefits of homeownership.

Bottom Line

If you can afford it, take control of your financial future by making homeownership part of your plan. It’s an investment you won’t regret.

Do you want to see what starter homes are available in our market? Let’s connect today to explore your options.

It’s no secret that affordability is tough with where mortgage rates and home prices are right now. And that may have you worried about how you’ll be able to buy a home. But, if you don’t need a ton of space, you may find you have more cost-effective options in an unexpected place: new home communities.

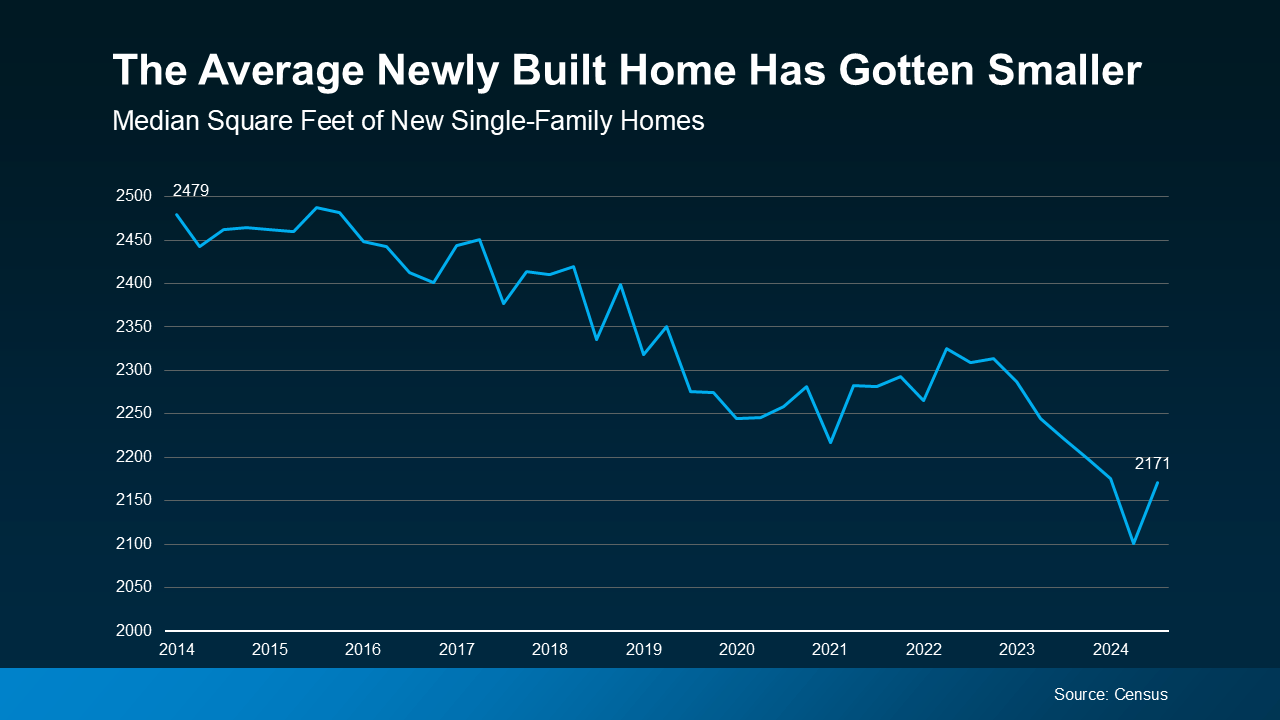

Builders Are Building Smaller Homes

Since smaller homes typically come with smaller price tags, buyers have turned their attention to homes with less square footage — and builders have shifted their focus to capitalize on that demand. As U.S. News notes:

“The combination of higher home prices and mortgage rates has strained a lot of people’s budgets. And that’s something builders recognize. To this end, they may be leaning toward smaller spaces . . .That, in turn, can lead to savings for buyers.”

Data from the Census shows the overall builder trend toward smaller, single-family homes has been over the last couple of years (see graph below):

As the graph shows, the average size of a brand-new home has dropped from 2,309 square feet in Q3 2022 to 2,171 square feet in Q3 2024. That’s a difference of 138 square feet.

As the graph shows, the average size of a brand-new home has dropped from 2,309 square feet in Q3 2022 to 2,171 square feet in Q3 2024. That’s a difference of 138 square feet.

At the end of the day, builders want to build what they know will sell. And the number one thing homebuyers are looking for right now is less expensive options to help offset today’s affordability challenges. As Multi-Housing News notes:

“The growing trend toward smaller homes is evident. These homes are less expensive to build and more attainable for many middle-income families, meeting both housing needs and modern lifestyle preferences.”

The Benefits of These Brand-New Homes

So, if you’re having trouble finding a home in your budget, it might be worth exploring newly built homes with a smaller footprint.

Not to mention, since newly built homes come with brand new everything, they have fewer maintenance needs and some of the latest features available, like energy-efficient appliances and HVAC. That’ll help you save on repair costs and your monthly utility bills. Sounds like an all-around win.

Bottom Line

Today’s builders are focusing their efforts on smaller homes at lower price points. That could give you more opportunity to find something that fits your budget. If you’re planning to buy soon, let’s connect to explore what’s on the market in your area and get your homeownership goals over the finish line.

Knowing what to budget for when buying a home may feel intimidating — but it doesn’t have to be. By understanding the costs you may encounter upfront, you can take control of the process.

Here are just a few things experts say you should be thinking about as you plan ahead.

1. Down Payment

Saving for your down payment is likely top of mind. But how much do you really need? A common misconception is that you have to put down 20% of the purchase price. But that’s not necessarily the case. Unless it’s specified by your loan type or lender, you don’t have to. There are some home loan options that require as little as 3.5% or even 0% down. An article from The Mortgage Reports explains:

“The amount you need to put down will depend on a variety of factors, including the loan type and your financial goals. If you don’t have a large down payment saved up, don’t worry—there are plenty of options available . . .”

A trusted lender will go over the various loan types with you, any down payment requirements on those, and down payment assistance programs you may qualify for. The more you know ahead of time, the easier the process will be. And the key to getting the information you need is working with a pro to see what’ll work best for your situation.

2. Closing Costs

Make sure you also budget for closing costs, which are a collection of fees and payments made to the various parties involved in your transaction. Bankrate explains:

“Mortgage closing costs are the fees associated with buying a home that you must pay on closing day. Closing costs typically range from 2 to 5 percent of the total loan amount, and they include fees for the appraisal, title insurance and origination and underwriting of the loan.”

When it comes to closing costs, a trusted lender can guide you through specifics and answer any questions you may have. They can also give you a better idea of how much you should be prepared to pay so you can cruise through your closing with confidence.

And as you plan ahead for closing day, be sure to budget for your real estate agent’s professional service fee too, in case the seller doesn’t cover it. But don’t worry, you’ll work with your agent ahead of time to agree on what this is, so you won’t be surprised at the finish line.

3. Earnest Money Deposit

And if you want to cover all your bases, you can also consider saving for an earnest money deposit (EMD). According to Realtor.com, an EMD is typically between 1% and 2% of the total home price and is money you pay as a show of good faith when you make an offer on a house.

But, it’s not an added expense. Instead, it works like a credit and goes toward some of your upfront costs. You’re simply using some of the money you’ve already saved for your purchase to show the seller you’re committed and serious about buying their house. Realtor.com describes how it works as part of your sale:

“It tells the real estate seller you’re in earnest as a buyer . . . Assuming that all goes well and the buyer’s good-faith offer is accepted by the seller, the earnest money funds go toward the down payment and closing costs. In effect, earnest money is just paying more of the down payment and closing costs upfront.”

Keep in mind, this isn’t required, and it doesn’t guarantee your offer will be accepted. It’s important to work with a real estate advisor to understand what’s best for your situation and any specific requirements in your local area. They’ll advise you on what moves you should make so you can make the best possible decisions throughout the buying process.

Bottom Line

The key to a successful homebuying savings strategy? Being informed about what you need to save for. Because, when you understand what to expect, you can plan ahead. With an expert agent and a trusted lender, you’ll have the information you need to move forward with confidence.

You may have heard that staging your home properly can make a big difference when you sell your house, but what exactly is home staging, and is it really worth your time and effort?

Here are a few quick FAQs that can help you decide how much you should prioritize staging as you prep for your move.

What Is Home Staging?

Staging is the process of arranging and decorating your house to highlight its best features and make it as appealing as possible to potential buyers. It can range from simple touch-ups to more extensive setups, depending on your needs and budget.

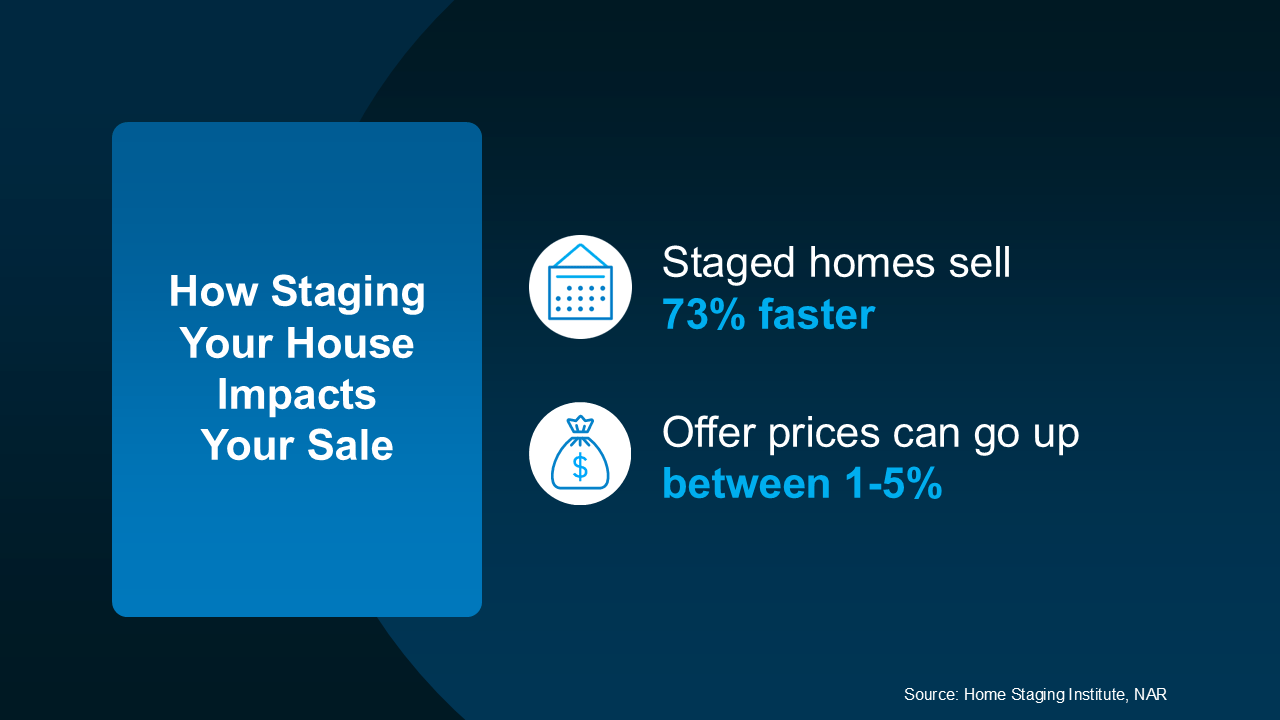

How Does It Help Me Sell My House?

Studies show good staging does have an impact on your sale. Staging your house well can help you attract more attention from buyers, which ultimately helps it sell faster and maybe for a higher price than an unstaged home (see visual):

What Are My Staging Options?

What Are My Staging Options?

Now that you see the value, let’s think through your options. The most common is leaning on your agent for their expert advice. They know what buyers like because they’re in showings all the time and hear that feedback first-hand. That expertise is crucial to getting your house market-ready. Basic staging with an agent usually means they give you insight into how you should:

- Declutter and depersonalize by removing photos and personal items

- Arrange your furniture to improve the room’s flow and make it feel bigger

- Add plants, move art, or re-arrange other accessories

Full-service staging is another option if your house needs more hands-on attention. This is when you hire a staging professional or staging company to come in, make recommendations, and do the work for you. Going this route is more involved and that makes it more costly too. That’s because it can include renting furniture and decor to more fully transform a space.

How Do I Know Which One To Pick?

Not sure which one you need? You don’t have to figure that out on your own. Your real estate agent will help determine what level of staging will make the most impact on your house and market.

They can help you decide if professional staging is worth the investment, or if you can knock it out with their advice alone. And just so you know, here are some of the factors an agent will look at to figure that out:

- Market Conditions: If the market is slower, going all in on staging can make your home look move-in ready and attractive to buyers who may otherwise be hesitant. If your local market is very active and homes are selling fast, you may be able to get by with doing less.

- Your Home’s Condition: If your home is vacant or has a unique layout, using a professional stager who can bring in the right furniture and accessories may help buyers truly visualize its full potential.

- Your Budget: Talk to your agent to get an idea of staging costs in your area, as it can be the difference between your house selling and sitting. But if your budget is tight or your home only needs minor updates, your real estate agent can help you think outside of the box by suggesting simple DIY staging tips to help your home look its best.

Bottom Line

Staging your house properly can make it much more attractive to buyers, but it’s not a one-size-fits-all solution, and every home shines differently. Let’s connect to talk through what your home really needs to stand out and sell for top dollar.

Fairfield

1205 Utah Street

3 Bedrooms, 1 baths, 1,437 sq. ft.

Offered for $499,000

FOR SALE

→ 1205 Utah Street

$499,000

- MLS#: 324113772

- Bedrooms: 3

- Baths: 1

- Sq. Ft.: 1,437

- Lot Size: 6,970 sq. ft.

- Year Built: 1951

- Laminate Wood Flooring

- Freshly painted

- Spacious Layout

- Fireplace

- Separate Living

- Large Bonus-Family Room

- New Carpet

- Recently remodeled Kitchen

- Stainless Steel Appliances

- Kitchen Nook

- Large Backyard

- Wood Deck

- Prime Location

- Fairfield Terrace Subdivision

- Updated Windows

- Minutes from Transportation

Welcome to 1205 Utah St, a beautifully updated 3-bedroom, 1-bathroom home in the heart of Fairfield. This inviting residence boasts a spacious layout with fresh new carpet and paint throughout, offering a clean and modern feel. Step inside to discover a bright living area that flows effortlessly into the kitchen and dining spaces, perfect for everyday living and entertaining.

The generously-sized bonus room is a standout feature, providing versatile space for a home office, playroom, or entertainment area. With direct access to the backyard, this room offers the ideal connection between indoor and outdoor living. This home was thoughtfully updated just a few years ago, ensuring that it's move-in ready and stylishly appointed.

Located in a prime location, you're just moments away from shopping, dining, and transit options, making commuting and running errands a breeze. Whether you're a first-time homebuyer or looking for a comfortable place to settle down, this home has it all!

")

")

COMMUNITIES

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Solano County is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

Each community is unique and offers a variety of lifestyle living. From the heart of the vines, to the small downtowns, to the waterfront and rolling hills discover your next destination.

Yountville

Yountville, in Napa Valley, is a luxurious getaway with small-town charm, renowned for its Michelin-starred dining, artsy attractions, and prestigious vineyards, best explored on foot or bicycle.

Vallejo

Boasting a thriving arts and culture scene, with numerous galleries, theaters, and music venues to explore and housing options, ranging from charming historic homes to modern waterfront condos, Vallejo provides something for everyone.

Benicia

Where tree-lined streets are dotted with boutiques, art galleries, and cozy cafes. Take a leisurely stroll along First Street, pausing to admire the architecture or indulge in farm-to-table cuisine at one of the local eateries.

Napa

The best things in life are the experiences we share, savor, and discover. Nowhere is that more apparent than in Napa Valley, where anyone – and everyone – can experience a taste of the good life.

VACAVILLE

From its convenient location midway between Sacramento and San Francisco to its diverse housing options and strong sense of community, Vacaville offers residents the best of both worlds.

CALISTOGA

Calistoga is famous for its geothermal hot springs and luxurious spas. The town's charming Lincoln Avenue offers eclectic shops, fine dining, and a vibrant Arts Walk, all within walking or biking distance.

AMERICAN CANYON

WHO YOU WORK WITH MATTERS

A new market to navigate, a new way to buy and sell,

a new way home.

The language of home is universal. It is the place where you are most known and most comfortable, where life unfolds and your story begins. Home is where you discover the extraordinary in the everyday. At Navigate Real Estate, we believe that "Every home has a story," and our mission is to help you tell yours. No matter where you are in your journey, Navigate Real Estate is an invaluable ally in your home buying and selling experience.

Wherever you're going... We'll get you there!

We see home as more than a house, so we approach real estate as more than a transaction. It's how we build relationships - by making people feel happy and confident about the biggest investment of their lives. This is more than our profession; it's our passion because our family never forgets how much home truly means to you and your family. So when you're ready for your next moment or your next adventure, call Alicia, she'll help you get there.

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

GOT QUESTIONS?

Get in Touch With Alicia

Suisun City

518 Arroyo Granda Lane

3 Bedrooms, 2.5 baths, 2,460 sq. ft.

Offered for $640,000

FOR SALE

→ 518 Arroyo Grande Ln., Suisun City

$640,000

Napa

1512 Juanita Court

4 Bedrooms, 2 baths, 1,587 sq. ft.

Offered for $899,000

COMING SOON

→ 1512 Juanita Court

$899,000

- MLS#: 324113054

- Bedrooms: 4

- Baths: 2

- Sq. Ft.: 1,587

- Lot Size: 12,375 sq. ft.

- Year Built: 1975

- Luxury LPV Flooring

- Wood Beams

- Vaulted Ceilings

- Dual Fireplace

- Separate Living/ Formal Dining

- New Fixtures Throughout

- Brand New Kitchen

- Stone Countertops

- Stainless Steel Appliances

- New Windows

- Paid For Solar

- Wood Mantel

- Lots of Natural Light

- Breathtaking Views of Surrounding Hills

- Blank Canvas Backyard

- Near Napa Wineries

- World Class Destination

- Open Concept

Welcome to your dream home in the heart of Napa Valley! This beautifully remodeled 4-bedroom, 2-bathroom residence seamlessly blends modern luxury with timeless charm, offering an unparalleled lifestyle in one of California’s most iconic destinations. Nestled on a private court in a highly sought-after Napa neighborhood, this home is more than just a place to live—it’s your gateway to the extraordinary Napa Valley experience.

As you step inside, you’ll be captivated by the stunning open-concept design, featuring a chef’s kitchen adorned with premium finishes, gleaming countertops, and a striking wood-beamed ceiling that radiates warmth and character. The wrap-around gas fireplace serves as the heart of the home, creating a cozy ambiance and a focal point that connects both the formal dining area and the inviting family room. Natural light pours through the space, highlighting the seamless flow ideal for entertaining or relaxing after a day exploring the valley.

Approaching the property, you’ll be greeted by breathtaking views of Napa’s iconic rolling hills, a picturesque reminder of the world-class setting that surrounds you. The expansive backyard is a blank canvas for your dreams—imagine adding a sparkling pool, designing a serene outdoor entertainment oasis, or simply savoring quiet moments under the Napa sky. Practicality meets convenience with a paid-off solar system for energy efficiency and ample RV parking for all your adventures.

Location is everything, and this home delivers! You’re just minutes from the vibrant heart of downtown Napa, where Michelin-starred dining, boutique shopping, and wine-tasting rooms beckon. Spend your weekends savoring world-renowned vintages at nearby estates like Domaine Carneros and Beringer Vineyards, or enjoy a farm-to-table meal at local favorites such as Oxbow Public Market, The French Laundry, or Mustards Grill.

For those who love the outdoors, Napa offers endless possibilities. Explore scenic trails by foot or bike through Skyline Wilderness Park or the Napa Vine Trail. Take a leisurely hot air balloon ride for unforgettable views of the valley, or enjoy a day of kayaking on the Napa River.

Families will appreciate Napa’s excellent schools, making this home a wonderful choice for primary residents, while second-home buyers will relish in owning a slice of paradise in this globally recognized vacation destination.

From its stunning design to its prime location, this property offers not just a home but a lifestyle—one filled with exceptional beauty, community charm, and the unmatched magic of Napa Valley. Welcome to your perfect blend of luxury, comfort, and adventure in wine country living!

COMMUNITIES

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Solano County is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

Each community is unique and offers a variety of lifestyle living. From the heart of the vines, to the small downtowns, to the waterfront and rolling hills discover your next destination.

Yountville

Yountville, in Napa Valley, is a luxurious getaway with small-town charm, renowned for its Michelin-starred dining, artsy attractions, and prestigious vineyards, best explored on foot or bicycle.

Vallejo

Boasting a thriving arts and culture scene, with numerous galleries, theaters, and music venues to explore and housing options, ranging from charming historic homes to modern waterfront condos, Vallejo provides something for everyone.

Benicia

Where tree-lined streets are dotted with boutiques, art galleries, and cozy cafes. Take a leisurely stroll along First Street, pausing to admire the architecture or indulge in farm-to-table cuisine at one of the local eateries.

Napa

The best things in life are the experiences we share, savor, and discover. Nowhere is that more apparent than in Napa Valley, where anyone – and everyone – can experience a taste of the good life.

VACAVILLE

From its convenient location midway between Sacramento and San Francisco to its diverse housing options and strong sense of community, Vacaville offers residents the best of both worlds.

CALISTOGA

Calistoga is famous for its geothermal hot springs and luxurious spas. The town's charming Lincoln Avenue offers eclectic shops, fine dining, and a vibrant Arts Walk, all within walking or biking distance.

AMERICAN CANYON

WHO YOU WORK WITH MATTERS

A new market to navigate, a new way to buy and sell,

a new way home.

The language of home is universal. It is the place where you are most known and most comfortable, where life unfolds and your story begins. Home is where you discover the extraordinary in the everyday. At Navigate Real Estate, we believe that "Every home has a story," and our mission is to help you tell yours. No matter where you are in your journey, Navigate Real Estate is an invaluable ally in your home buying and selling experience.

Wherever you're going... We'll get you there!

We see home as more than a house, so we approach real estate as more than a transaction. It's how we build relationships - by making people feel happy and confident about the biggest investment of their lives. This is more than our profession; it's our passion because our family never forgets how much home truly means to you and your family. So when you're ready for your next moment or your next adventure, call Alicia, she'll help you get there.

WHY NAVIGATE REAL ESTATE

If you live here already, you know how blessed we are. If you're considering living or investing here, you've probably experienced some of the area's extraordinary possibilities: country settings and small-town communities; enthralling agricultural beauty, and true farm to fork lifestyle, If Northern California is your real estate destination, you've arrived at the right spot. Whether you're looking to buy your first home - or to sell an estate - expect nothing less from us than a Meritage blend of real estate expertise, professional service, creativity, and a passion for achieving your goals.

GOT QUESTIONS?

Get in Touch With Alicia

Suisun City

518 Arroyo Granda Lane

3 Bedrooms, 2.5 baths, 2,460 sq. ft.

Offered for $640,000

FOR SALE

→ 518 Arroyo Grande Ln., Suisun City

$640,000

When planning a move, a newly built home might not be the first thing that comes to mind. But with more brand-new homes on the market and builders focusing on smaller, more affordable options, this type of home may just be the key to crossing the homebuying finish line.

Here’s why a new build is worth considering – and how an agent can help you find one that meets your needs and your budget.

1. More Newly Built Homes Are Available Right Now

First, let’s break down the types of homes on the market. A newly built home is a house that was just built or is under construction. On the other hand, an existing home is one a homeowner has already lived in.

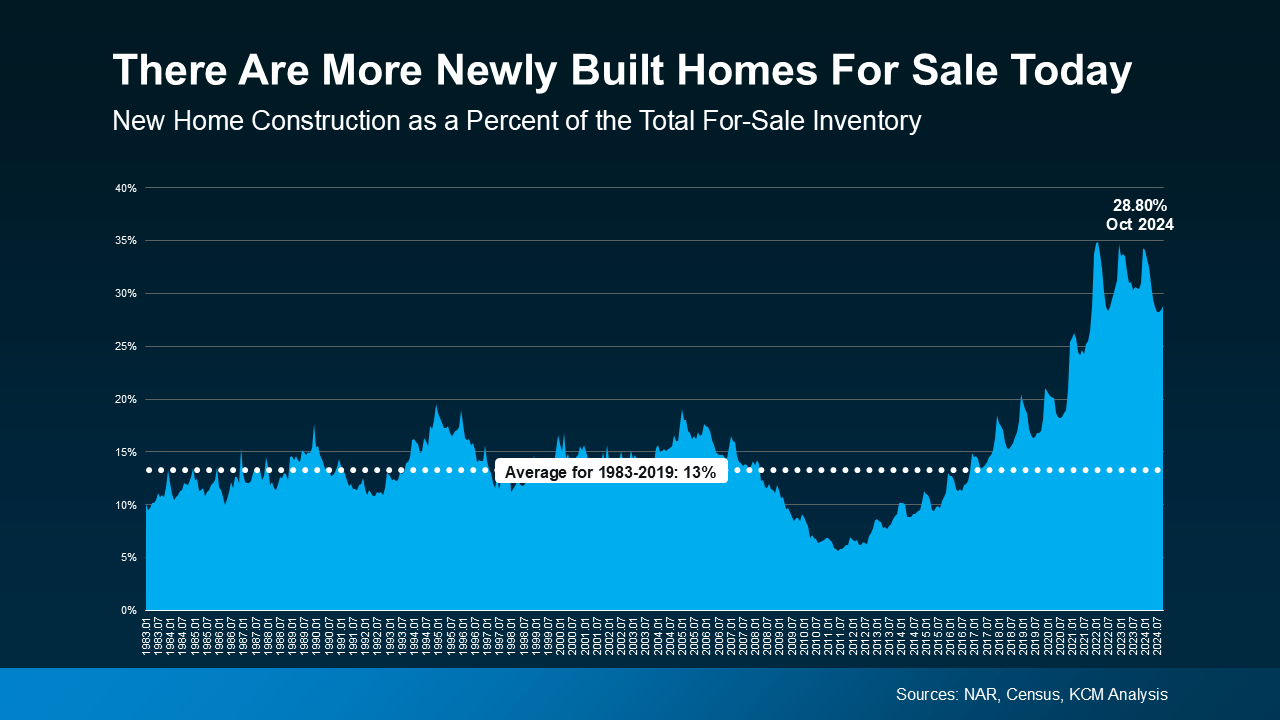

Right now, the number of existing homes for sale is still low. And, if you’re struggling to find something you like because there aren’t that many existing homes for sale, opening up your search to include brand-new homes could really expand your options. That’s because there are more newly built homes available right now than in a typical year (see graph below):

From 1983 to 2019, newly built homes made up only 13% of the total inventory of homes for sale. Today, that number has climbed to 28.8%, according to the most recent data.

From 1983 to 2019, newly built homes made up only 13% of the total inventory of homes for sale. Today, that number has climbed to 28.8%, according to the most recent data.

And as Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), notes:

“Even though existing home sales have been stuck at low levels, newly constructed home sales look to mark one of its best annual performance in 15 years . . . The new home inventory has been consistently rising with homebuilders getting active and making up around 1/3 of total inventory.”

While the uptick in new home construction is encouraging, rest assured that builders aren’t overdoing it, they’re just making up for over a decade of underbuilding. There are still way more buyers than there are homes on the market. But the good news for you is this increase in newly built homes means more options for your search.

2. Newly Built Homes Are Becoming Less Expensive

Still skeptical if a new build is right for you or if they’re even in your budget? The average cost of newly built homes has actually come down from a year ago.

Why is that? Builders know affordability is top of mind for homebuyers right now. So they’re focusing their efforts on building smaller homes they can offer at lower price points and are more likely to sell. As Realtor.com says:

“Builders are increasingly bringing smaller, more affordable homes to the market, so buyers may find more newly-built homes that fit their budget.”

Something to keep in mind: buying a newly built home isn’t the same as buying an existing one. Builder contracts have different fine print. So be sure to partner with a local agent who knows the market, builder reputations, and what to look for in those contracts.

Bottom Line

Depending on your needs and budget, a new build might be the opportunity you’ve been waiting for to bring your homebuying vision to life. If you’re interested in a brand-new home, let’s connect so you can check out what builders in your area are up to.

ALICIA DENSON

REALTOR®

Managing Partner

707.509.0892

aliciamdenson@gmail.com

DensonGroupre.com

DRE Lic# 02068650

DRE Lic# 02221115

Made with ❤️ by navi © 2024